How Secondaries Are Shaping Asia’s Private Equity Future

The Secondary Market Boom of 2024: Unveiling Key Investment Opportunities

October 3, 2024

Rising Debt, Shifting Markets: A Look at G7 Fiscal Trends through 2029

October 3, 2024

The private equity (PE) market in Asia is experiencing a noticeable shift, with GP-led secondary transactions becoming an increasingly popular tool for managing liquidity. As traditional exit strategies, like IPOs, lag in the region, the secondary market is stepping in to fill the gap. Countries like India and China are witnessing large-scale secondary transactions, signalling a growing acceptance of this alternative liquidity pathway.

With the global private equity market facing increasing volatility and uncertainty, understanding how the secondary market is evolving in Asia is essential for investors looking to capitalize on new opportunities.

GP-Led Secondaries: A Strategic Response to Challenging Exit Environments

Traditionally, private equity firms (GPs) and their portfolio companies relied on exits via IPOs or trade sales to provide returns to investors. However, over the past few years, challenging market conditions and regulatory hurdles have slowed the pace of IPOs in Asia. This has led to a growing reliance on GP-led secondary transactions, where the GP facilitates the sale of assets or interests within a fund, providing liquidity to investors without needing a full exit.

These transactions offer a viable alternative for liquidity, allowing GPs to extend the holding period of their most valuable assets while still providing returns to early investors. In markets like China and India, where IPO timelines are becoming increasingly uncertain, secondary transactions have become an essential tool for navigating the complexities of exit planning.

Secondary Transaction Volumes on the Rise in Asia

The growing importance of secondaries is reflected in the rising transaction volumes across Asia. In 2023, secondary transaction volumes increased to US$5.5 billion, up from US$5.25 billion in 2022. While the overall growth may appear modest, the consistent upward trend highlights a gradual shift in the mindset of investors and market participants in the region.

The rise in secondary transactions is also fueled by an increasing willingness among investors to explore alternative liquidity options, particularly as they seek to avoid the risks associated with delayed or failed IPOs. With Asia’s maturing private equity market, investors are becoming more comfortable with the idea of recycling capital through secondary transactions, ensuring steady returns even when traditional exits are not feasible.

The Untapped Potential of Asia’s Secondary Market

Despite the growing activity in the region, the secondary market in Asia remains relatively underdeveloped compared to other global markets. In 2023, global fundraising for secondary funds reached a staggering US$118 billion, yet only 5-10% of this capital was allocated to Asia. This indicates a significant opportunity for growth, as both institutional investors and private equity firms recognize the untapped potential of the Asian secondary market.

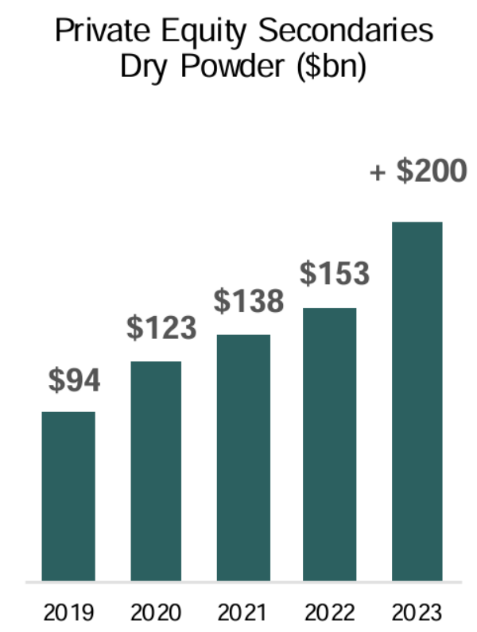

With more dry powder i.e. unused committed capital, waiting to be deployed in private equity secondaries, investor interest is clearly high. In fact, the global reserve of dry powder for secondary transactions surpassed US$200 billion in 2023, signalling that investors are poised to increase their exposure to this segment of the market. For Asia, this presents a compelling opportunity as secondary market infrastructure and transaction activity continue to develop.

Strong Investor Demand Fuels Confidence

The increasing volume of dry powder available for secondaries reflects strong investor demand and confidence in the asset class. Investors are recognizing that secondary transactions provide not only liquidity but also an opportunity to gain exposure to high-quality assets at potentially attractive valuations. With this growing pool of capital, the secondary market is well-positioned to continue expanding across Asia.

According to Coller Capital’s latest Global Private Capital Barometer, 38% of respondents plan to increase their investments in secondaries within the next year, making it the second most popular strategy in private markets. This shift in investor sentiment is significant, as it indicates that secondaries are becoming a mainstream component of private equity portfolios, particularly in regions like Asia where liquidity options are limited.

The Role of GP-Led Transactions in Asia’s Future

As market conditions in Asia evolve, GP-led secondary transactions are expected to play an even more critical role in the private equity ecosystem. Sponsors are increasingly turning to these transactions to manage their portfolios and provide liquidity to investors, particularly in an environment where market volatility and economic uncertainty continue to challenge traditional exit routes.

The ability to extend the life of funds, offer liquidity to investors, and retain ownership of key assets makes GP-led secondaries an attractive option for both GPs and limited partners (LPs). This dynamic has created a positive feedback loop, where the success of secondary transactions leads to more GPs considering them as a viable strategy, further fuelling market growth.

Outlook: Growth and Development of Asia’s Secondary Market

The outlook for secondary transactions in Asia remains highly optimistic. With the continued focus on liquidity and the challenges posed by the region’s IPO market, more sponsors are expected to tap into the secondaries market as a way to deliver returns to investors. This trend suggests that secondary transactions will become an increasingly important tool for managing liquidity and generating value in Asia’s private equity market.

Moreover, as global investors allocate more capital to the region, the secondary market in Asia is likely to see accelerated growth. Increased awareness and acceptance of secondary transactions, coupled with the region’s growing pool of investable assets, create a fertile ground for future expansion.

For investors, this presents a unique opportunity to gain exposure to high-quality assets in a market that is still in the early stages of development. As secondary transactions continue to gain momentum, those who recognize and capitalize on this emerging trend will be well-positioned to benefit from the growth of Asia’s private equity landscape.

Conclusion: A Growing Opportunity for Investors

The rise of GP-led secondary transactions in Asia’s private equity market reflects a broader shift in how liquidity is managed in the region. As traditional exits like IPOs become less reliable, secondary transactions offer a stable and effective alternative for investors seeking liquidity. With transaction volumes on the rise and increasing global interest in Asia’s private equity market, secondaries are emerging as a key area of growth.

For investors, understanding the dynamics of this evolving market is essential to unlocking new opportunities and capitalizing on the potential for future returns. As more sponsors turn to secondaries to manage liquidity, the stage is set for continued expansion and development across Asia’s private equity landscape.

{kind=link}

{kind=link}

{kind=link}