ESG Funds Capture Over 20% of Private Capital Fundraising in 2024

The Magnificent Seven-A Tale of Unprecedented Growth and Market Dominance

September 3, 2024

The Secondary Market Boom of 2024: Unveiling Key Investment Opportunities

October 3, 2024

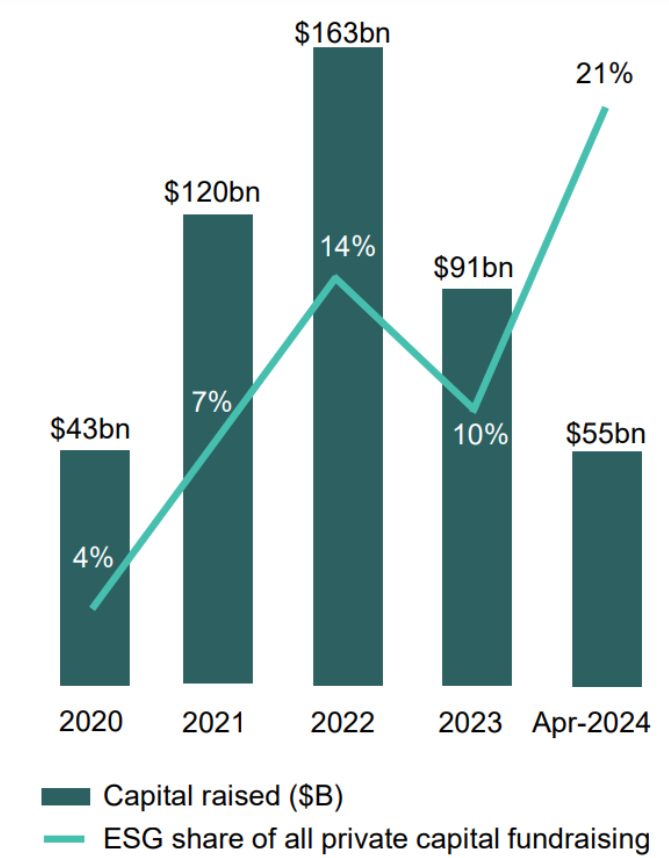

As of April 2024, Environmental, Social, and Governance (ESG) funds have secured more than 20% of all private capital fundraising, marking a significant milestone in the investment landscape. This trend underscores the growing importance of sustainable and responsible investing in the private markets sector.

The Rise of ESG Fundraising

ESG fundraising reached unprecedented heights in 2022, defying challenging macroeconomic conditions across alternative investments. This success demonstrated the ability of ESG funds to differentiate themselves and capture investor attention. However, the landscape shifted in 2023 as rising interest rates and pressure across investment portfolios led some investors to reassess their ESG priorities.

Despite these challenges, ESG fundraising has shown resilience in 2024. By the end of April, ESG funds had already raised US$55 billion, matching the impressive pace set in 2022. This rebound suggests that investor interest in ESG-focused strategies remains strong, even in the face of economic uncertainties. Europe has dominated impact fundraising so far this year, increasing its share of aggregate capital raised from 67% in 2023 to 79% by April 2024.

Performance Comparison: ESG vs. Non-ESG Funds

Recent data indicates that the performance of private ESG funds is comparable to that of non-ESG private funds. A study examining 215 ESG funds and 10,812 non-ESG funds revealed that the average internal rate of return (IRR) for ESG funds was 13.5%, 1.5% slightly lower than the 15% IRR for non-ESG private capital funds.

Interestingly, ESG funds exhibited lower variance in their returns, suggesting they may be better equipped to manage downside risks. This characteristic could make ESG funds more attractive to investors seeking consistent performance and stability in their portfolios over time.

Drivers of ESG Fund Growth

The robust growth in ESG fundraising across private markets indicates a growing trend among fund managers to align new funds with ESG requirements. This shift is driven by various factors, including increased capital raising potential, enhanced risk management capabilities and improved deal selection strategies.

As the ESG sector continues to evolve within alternative investments, its growth trajectory is expected to persist, particularly due to Europe’s more developed regulatory environment for sustainable finance.

Geographic Distribution of ESG Fundraising

Europe has emerged as the dominant force in impact fundraising in 2024. The region’s share of aggregate capital raised increased from 67% (US$15.0 billion) in 2023 to an impressive 79% (US$5.2 billion) by April 2024. This surge reflects Europe’s advanced regulatory framework and strong investor appetite for impact-focused investments.

In contrast, North America has taken the lead in climate funds, raising US$15.0 billion, or 82% of the global total, by April 2024. This regional disparity highlights the different focus areas and maturity levels of ESG investing across markets.

Dominant Asset Classes in ESG Fundraising

Private equity and infrastructure continue to dominate the ESG fundraising landscape. Collectively, these two asset classes accounted for 66% of all ESG funds raised (US$55 billion) in 2024 up to April, with private equity securing US$18.4 billion and infrastructure attracting US$17.9 billion.

The infrastructure sector, in particular, has seen a significant shift towards renewable energy investments. In 2023, a record 59% of infrastructure deals were in renewables. Moreover, since 2014, 72% of the US$1.23 trillion of capital raised with exposure to renewable energy came from infrastructure funds. This trend underscores the crucial role that infrastructure plays in the transition to a low-carbon economy.

Regulatory Environment and Future Outlook

The strong growth in ESG fundraising, especially in Europe, indicates that supportive regulatory environments and sustained investor interest are likely to continue driving the sector’s expansion. The European Union’s Sustainable Finance Disclosure Regulation (SFDR) and other similar initiatives have created a more structured framework for ESG investing, encouraging both fund managers and investors to prioritize sustainable strategies.

However, investors should remain mindful of changing macroeconomic conditions and their potential impact on ESG priorities. Factors such as inflation, interest rates, and geopolitical tensions could influence the allocation of capital to ESG funds in the short to medium term.

Conclusion

The significant share of private capital fundraising captured by ESG funds in 2024 marks a turning point in the investment landscape. As regulatory frameworks evolve and investor awareness grows, ESG considerations are likely to become increasingly central to investment decisions across all asset classes.

Fund managers and investors alike must navigate this changing landscape carefully, balancing the pursuit of financial returns with the imperative of creating positive environmental and social impact. As the ESG sector continues to mature, it will play an increasingly vital role in shaping the future of private capital markets and contributing to a more sustainable global economy.

{kind=link}

{kind=link}

{kind=link}