The Bustling Space Industry

The Opportunity in Private Debt

September 5, 2023

Retail Investors’ Focus and Behaviour in 2023

October 4, 2023

The Current Outlook

What was once the exclusive realm of covert government initiatives has now shifted into the control of forward-thinking billionaires and the private sector. In 2020, the announcement of commercial space tourism launches by several privately-owned companies marked a notable milestone in space technology awareness, arguably reaching levels not seen since the end of the Apollo missions in 1972.

By 2021, the global space industry had undergone significant expansion, boasting more than 10,000 private space technology companies, 5,000 major investors, 130 state organizations, and engaging across 20 diverse business sectors. Notable players in this surge were well-known entities like SpaceX, Blue Origin, and Virgin Galactic, leading the charge in the modern space race. This remarkable growth translated into the industry’s value nearly tripling from USD 110 billion to nearly USD 357 billion over the span of 15 years, from 2005 to 2020.

Space Industry is Becoming More Accessible

The space industry had always been dominated by government-sponsored programmes focusing on military capability until recently where private companies entering the industry and prioritizing operational efficiency. In 2022, there were 178 space missions, 90 of which were conducted by the private sector and 61 by SpaceX. Space tourism could really become more accessible to average person like you and me.

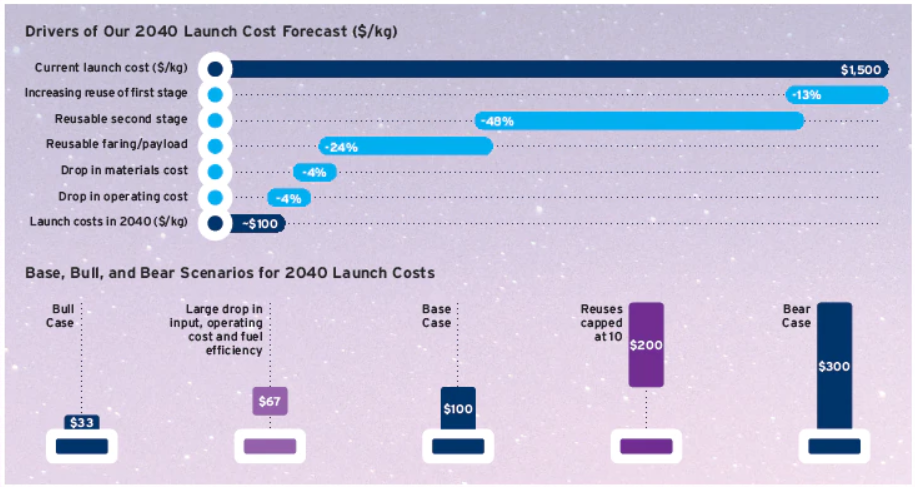

What brought about the sudden increase in accessibility to space were two key factors: the entrance of the private sector into the industry and a significant reduction in launch costs. As of today, the cost of launching into space, at USD1,500/kg, is approximately 30 times less than the price of a NASA Space Shuttle launch back in 1981. This significant cost reduction is attributed to several factors, including the development of reusable rockets and launch vehicles, the utilization of innovative materials and fuels, more efficient production techniques, and advancements in robotics and electronic systems.

According to Citi GPS report, there is potential for launch costs to decline even further, potentially reaching as low as USD100/kg by 2040 driven by reusability, scale, lower input cost and cost-efficient production methods. And in an optimistic scenario, dropping as far as USD33/kg.

Source: Citi Research

Investment in Space Industry

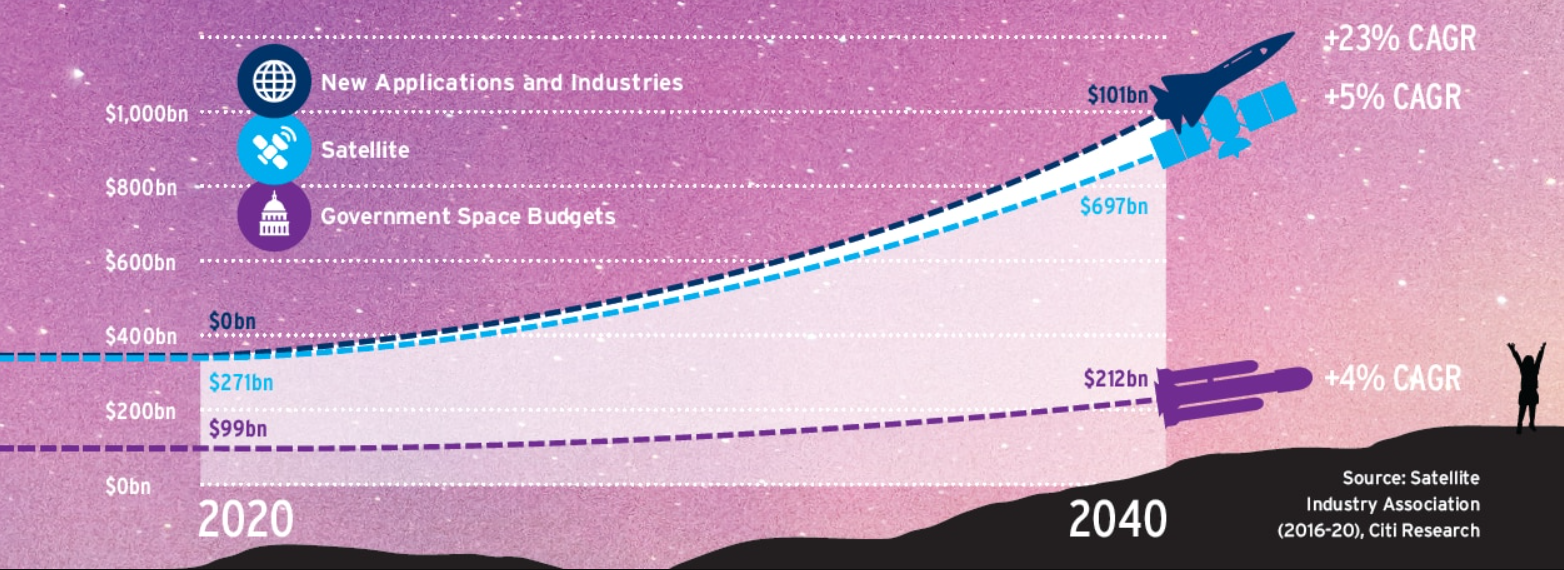

Investments in the space industry are experiencing significant growth. According to Citigroup’s analysis, the global space sector could reach a value of USD1.0 trillion by 2040, marked by a 5% compound annual growth rate starting from 2020. In an even more optimistic outlook, the Bank of America forecasts the industry to reach USD1.4 trillion by 2030. This growth will primarily be driven by increased revenue in manufacturing, launch services, and ground equipment within the satellite sector. However, the most rapid expansion is expected to come from emerging space applications and industries, with projected revenue surging from USD0 to USD101 billion over the given period.

Governments worldwide are also making substantial investments in the space industry, creating new opportunities for start-ups and investors. While the United States holds a prominent position, China is making notable strides, with reported investments of USD10.3 billion in 2021. Many other countries are also initiating their own space programs. Singapore is actively participating in the global space race, with its government allocating USD150 million for space technology research and development.

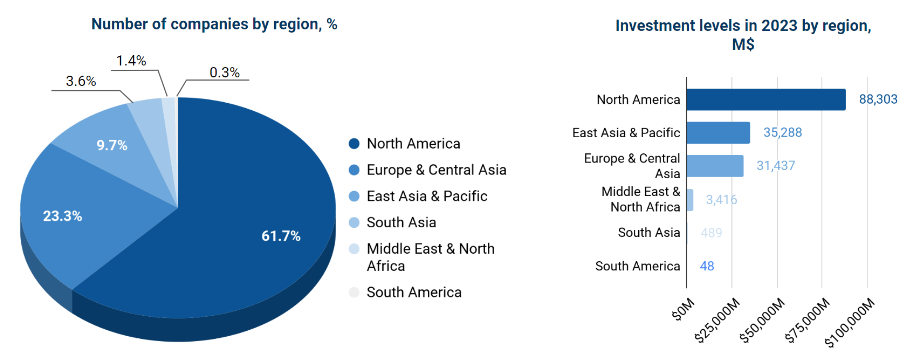

The US and Canada are the world leaders by the number of SpaceTech companies and levels of investment received so far in 2023. Meanwhile, East Asia and Europe have secured comparable levels of funding, although Europe has a higher number of companies operating in this field. Surprisingly, despite a relatively small share of companies, comprising just 1.4% of the total, the Middle East and North Africa region have attracted substantial investment, surpassing USD3.4 billion in total, positioning it as the fourth-largest recipient of space tech investment worldwide.

Source: https://www.deep-innovation.tech/deeptech-spacetech-dashboard

SpaceTech Related Companies to Watch Out For

With growing global interest in space exploration and the increasing demand for space infrastructure, the space industry is thriving. Emerging space technology companies are now competing to make significant strides in this dynamic sector. As mentioned, the key players in the market are SpaceX, Blue Origin, Virgin Galactic and NASA, to name a few, they are primarily from the west. Southeast Asia is somewhat slower to grow but is starting to catch up as well. According to a report by Frost & Sullivan, the Southeast Asia space industry market was valued at approximately USD2.27 billion in 2020 and is expected to reach USD3.77 billion by 2025.

Currently, there are 5 emerging spacetech companies in Southeast Asia, all based in Singapore, namely, SpeQtral, NuSpace, Aliena, Transcelestial and SpaceChain. In Malaysia, we also have a few spacetech companies and start-ups that are making their names known in the space industry i.e. SpaceIn, Angkasa-X, Independence-X Aerospace (IDXA).

As the space industry sector is rapidly growing and investments from global actively pouring in, there are opportunities lie within particularly in the space technologies area, a potential investment prospect that smart investors should watch out for. As always, it is advisable to carefully assess each investment option, conduct thorough research and consider seeking professional advice to make an informed decision that aligns with one’s objectives and investment goal before investing.

{kind=link}

{kind=link}

{kind=link}