End of Rate Hike Boosting Investor Confidence

Pyramid of Financial Risk

December 4, 2023

Insights: How Are Top Banks Investing in 2024?

January 2, 2024

In a pivotal move, the United States Federal Reserve has opted to maintain interest rates at the current target range of 5.25%-5.50% for the third consecutive meeting, signalling a potential conclusion to the most robust cycle of hikes in the past four decades. The decision suggests that the policy rate is expected to be lower by the close of 2024, with the median forecast indicating a decrease of three-quarters of a percentage point from the existing range. Notably, no officials foresee a rise in rates by the end of the upcoming year.

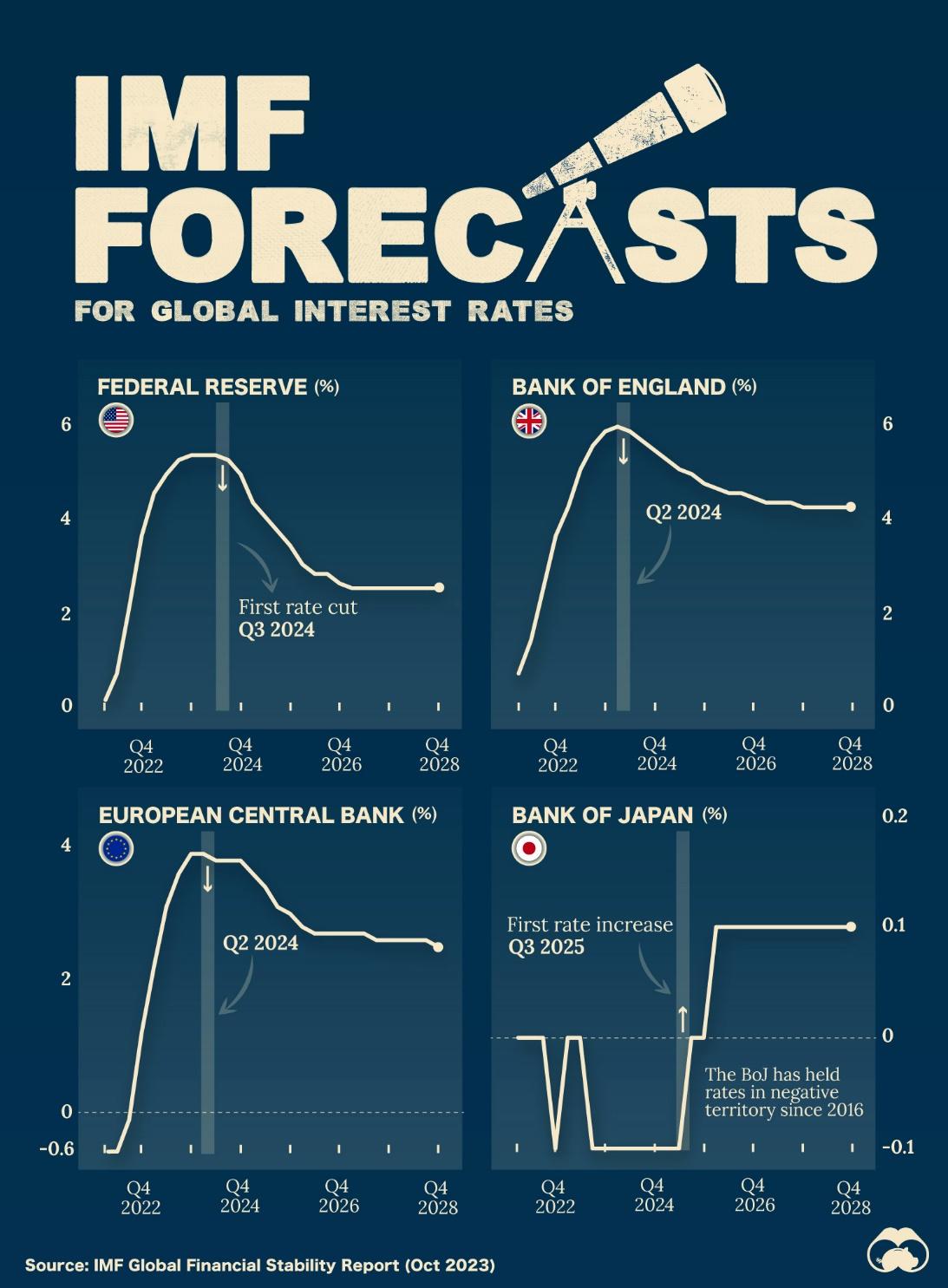

Other than the US, other advanced economy countries i.e. Europe, United Kingdom and Japan are projected to begin easing their interest rates gradually by mid of 2024. This projection by the International Monetary Fund (IMF) involves the central bank policy rates of the four major economies by using World Economies Outlook forecast data as of October 2023.

According the illustrated graph, the US is expected to see interest rates peak around 5.40% before rate cuts beginning to implement in Q3 2024. Both UK and Europe are expected to begin their rate cuts implementation earlier in Q2 2024 after seeing interest rates to peak around 5.90% and 3.80%, respectively.

Japan, on the other hand, has held interest rates at 0% or slightly lower since 2016. The country is poised to do the opposite of other central banks. Instead of cutting rates, IMF forecasted Japan to increase rates in 2025, making the country to see its first positive interest rates after 9 years. The Japanese economy as a whole has struggled over the past few decades with weak consumer demand and there is concern that the raising of interest rates might make the country’s economy recovery tougher in the long run.

Optimistic Outlook Ahead

The overall economic projections align closely with the envisioned “soft landing” scenario, a cornerstone for US central bankers who anticipate a gradual slowdown in inflation without the spectre of a recession or a significant surge in unemployment. This optimistic outlook has resonated positively in the financial markets, with the S&P 500, Dow Industrials, and NASDAQ Composite indices registering gains of 1.37%, 1.4%, and 1.38%, respectively. The Dow even achieved a record close.

The implications of the Federal’s decision extend beyond the stock market, promising a ripple effect in the broader economy. Lower borrowing costs are anticipated to stimulate increased private equity investments, foster higher start-up activity, and contribute to an overall strengthening of business confidence. As a result, private capital market investors are poised to encounter a growing array of opportunities to expand and fortify their portfolios in the wake of this pivotal moment in monetary policy.

{kind=link}

{kind=link}

{kind=link}